Tech Supercycle vs. The Fed: The 6-Month Playbook

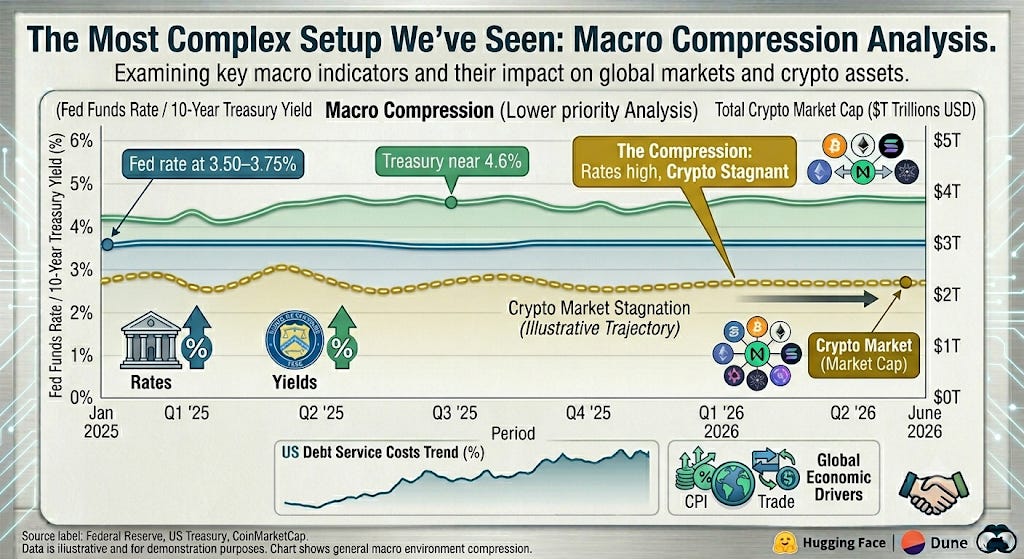

The Fed hasn’t moved, and the data isn’t giving it much reason to. Rates are still parked at 3.50- 3.75%, core PCE is still sticky, and the 10-year Treasury near 4.6% is paying institutional capital to sit still. So that’s what it’s doing. The $7 trillion in money markets isn’t lazy. It’s waiting for permission.

Bitcoin ETFs just logged a 10-day outflow streak, with net redemptions totaling close to $3 billion since May 15. M2 is at an all-time high. None of that money has found its way into risk assets.

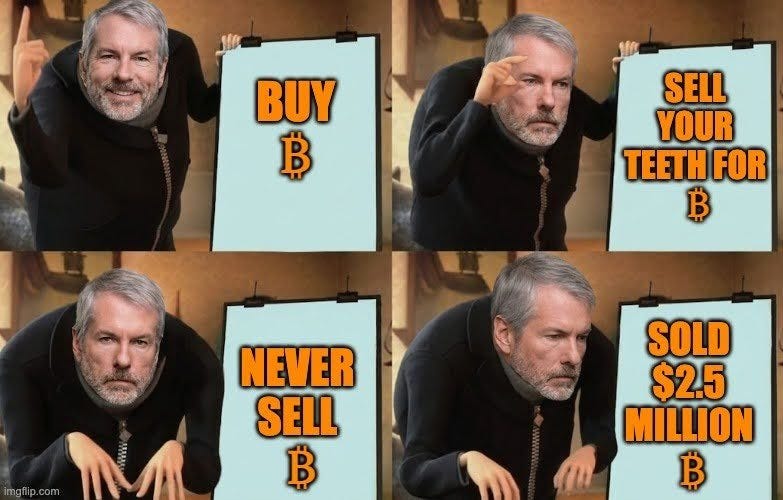

Even Saylor blinked. Strategy sold 32 Bitcoin this week, worth about $2.5 million. The amount barely registers in their holdings. The symbolism registers everywhere.

That permission the market is waiting for hasn’t come yet. And the path to it runs directly through the Strait of Hormuz.

Oil Prices, & Why They Matter More Than Wall Street Thinks

Recently on Bloomberg, analyst Mark Cudmore made an argument you’ve probably heard before. Why should he worry about oil prices when the AI and tech sector are delivering such incredible returns? The Bloomberg host called the setup asymmetric. We’d push back on that. What keeps energy prices elevated keeps the Fed from moving, and what the Fed does with rates determines when that $7 trillion in money markets finally moves into risk assets.

There’s something else Cudmore’s argument misses. The people choosing between gas and groceries in this economy aren’t participating in high-performing AI and tech IPOs. Oil prices aren’t a talking point for those families. They’re the monthly budget.

The picture shifted on May 28. Core PCE came in line. White House sources reported a tentative 60-day ceasefire with Iran. The war premium is starting to ease. A deal gives Warsh the cover he needs to move. We just don’t want to see this thing drag into midterms.

Worth noting: Iran has been accepting Bitcoin for oil shipments through the Hormuz Strait. The adversary is already settling in digital assets.

The Golden Lining: The Supercycle Running Alongside All of This

Here’s what the macro doesn’t touch.

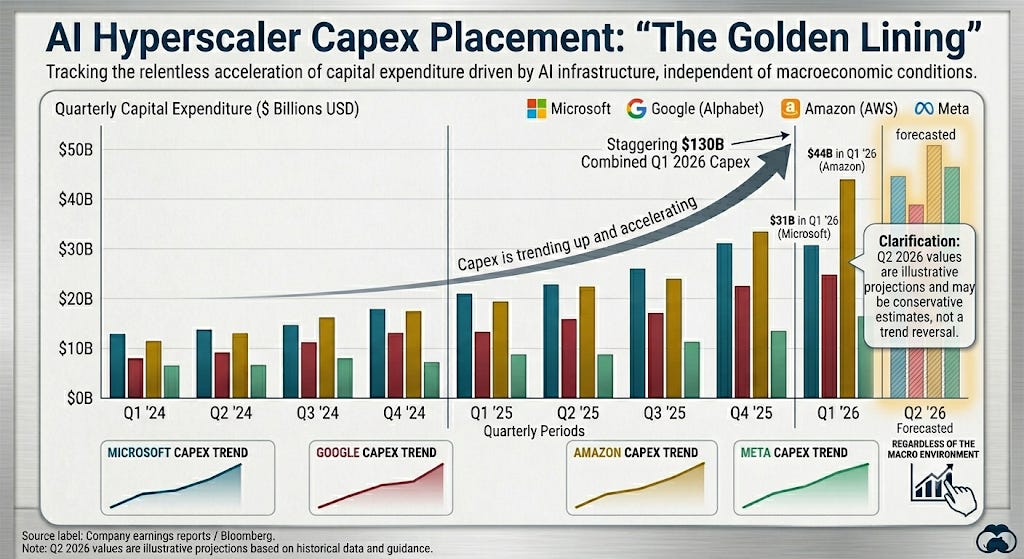

Corporate and venture capital allocation to physical AI infrastructure is running its own race, and it has been for months. Hyperscaler capex from Microsoft, Google, Amazon, and Meta isn’t waiting for a rate cut. The GPU supply crunch is structural and global. No FOMC meeting affects it.

The CLARITY Act is stalled. Even Trump is now creating friction. We’ve seen this play before. We’re not betting on the bill. We’re watching it.

The opportunity sitting in front of us for the next 6 months is specific: physical compute and scalable networks. Not application-layer narratives. The infrastructure on which the AI economy is being built.

The 6-Month Core Asset Allocation

The tier structure here reflects macro sensitivity, not conviction level. Both tiers are high-conviction plays. The difference is how each one behaves while we’re still waiting for the macro to cooperate.

TIER 1: RELATIVE OUTPERFORMERS: DePIN & Scale

Render Network (RENDER): The Hardware Pure-Play

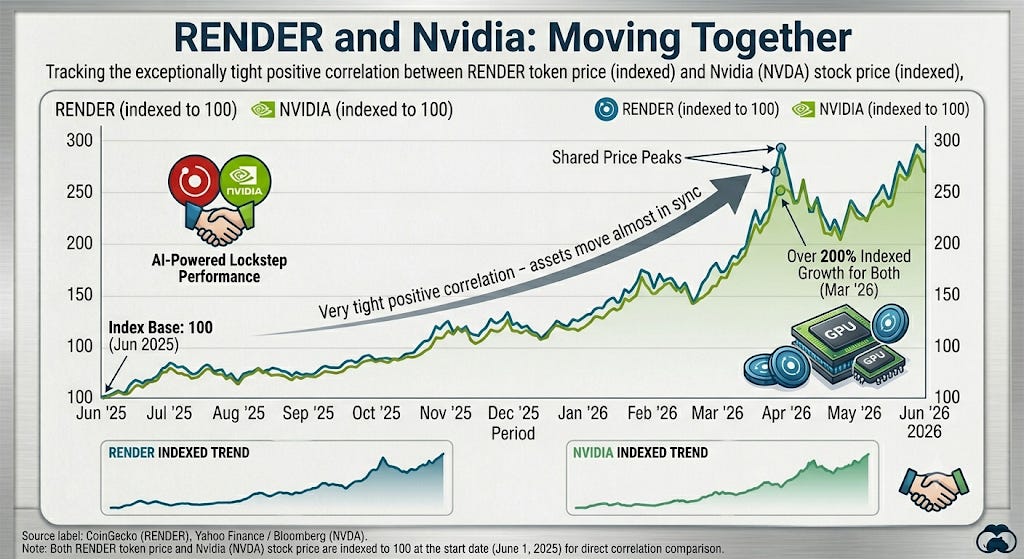

The GPU supply crunch is structural and it isn’t going away. Render connects idle enterprise-grade GPUs with real computational demand, and that demand exists completely independent of what the Fed does in September.

RENDER’s correlation with Nvidia isn’t a coincidence. When GPU demand runs, both run. We’ve been watching this since Sora dropped in February 2024. That’s also when the compute demand picture became hard to argue with. That thesis is still intact. Demand has only grown since then.

Consolidating defensively around the $2.00 baseline. That’s where we see the floor being established.

NEAR Protocol (NEAR): The Sovereign Data Layer

The co-founder of NEAR Protocol helped write the Transformers paper, the foundational architecture behind today’s major AI models. Credibility here starts at the foundation level and builds from there.

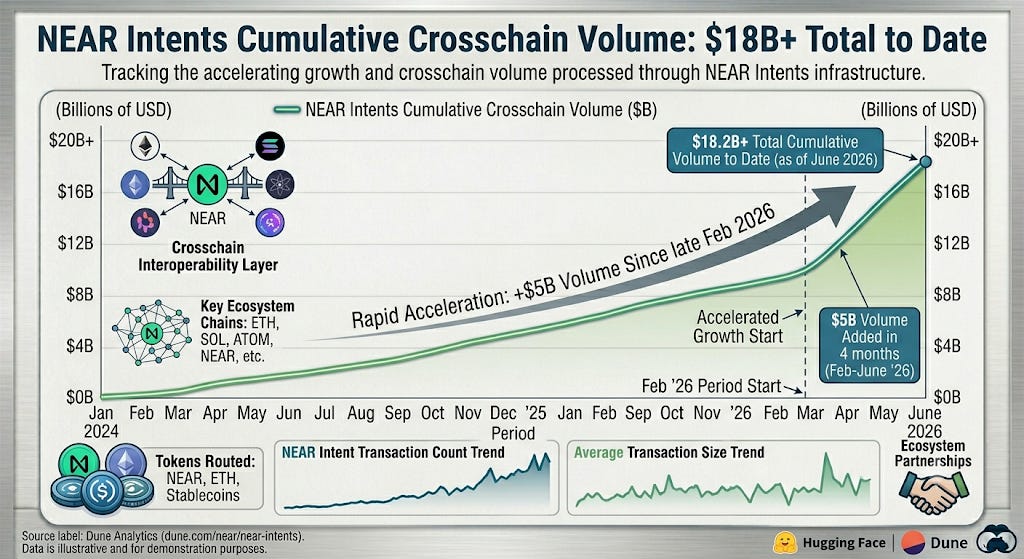

NEAR Intents has processed over $18 billion in cross-chain volume to date. $5 billion of that has come in just since late February 2026. This is in production and accelerating.

The NEAR AI suite (Cloud, Agent Hosting, the Agent Market, and the Confidential GPU Marketplace) is being built for the agentic economy that’s already arriving. AI agents need to move value privately across chains. NEAR is building the rails they’ll run on.

Arthur Hayes predicts that NEAR could grow 20x by next year. His case rests on exactly what we’ve been tracking: Intents as the privacy-native crosschain infrastructure for autonomous AI agents. Further, Grayscale’s research team has called this the “building mode” phase, the quiet period before the market fully prices it in.

Both pillars feed $NEAR buybacks directly. The token has more than doubled since March, and it’s sitting right around $2.60 as we write this.

TIER 2: MACRO-SENSITIVE ACCUMULATOR

Bittensor (TAO): The Institutional Blue-Chip

TAO is in a classic market transition: from speculative retail hands into long-term institutional accumulation. The 21-million supply cap mirrors Bitcoin’s. The multi-subnet marketplace is the most credible open-source alternative to the closed AI monopolies that the major tech platforms are building.

TAO is more macro-sensitive than the Tier 1 picks. It needs liquidity conditions to improve before it sprints. In the current environment, that means patience.

We expect TAO to consolidate within a $250–$350 range over the next 6 months as the subnet ecosystem works through its weaker teams and the institutional floor continues to build. This is a position you size and sit with.

iTrustCapital | Get $100 Funding Reward + No Monthly Fees when you sign up using our custom link! ➜ https://bit.ly/iTrustPaul

Strategy: Positioning for the Next 6 Months

Follow the compute, not the narrative. Physical infrastructure with measurable demand (GPU networks, scalable L1s with real TVL, open-source AI marketplaces) is where the supercycle is running.

Buy on Red, not on green. RENDER near $2.00, NEAR near $2.50, and TAO in the $250–$350 range are the levels we’re watching. Chasing all-time highs in a tight-liquidity environment is how portfolios get caught offside.

Keep two macro triggers on your radar. An Iran ceasefire resolution and CLARITY passing could unlock the $7 trillion sitting in money markets. If either one breaks favorably, risk-on will move fast. The infrastructure thesis doesn’t require either. Both would accelerate it.

Size TAO for patience. It’s the most macro-sensitive of the three. The institutional accumulation story is real, and it plays out over quarters. Treat it accordingly.

Stay diversified. The AI infrastructure buildout is real. Macro volatility is also real. Both things are true at the same time.

The Verdict: The Supercycle Doesn’t Need Permission

The macro is complicated. The AI infrastructure buildout isn’t.

Over the next 6 months, the portfolios positioned along physical compute and scalable networks will look very different from those that were waiting for the Fed to give them a green light. The supercycle doesn’t pause for rate decisions. The capital will catch up eventually.

We know which side we’d rather be on. How about you?

Earn rewards when you get started on OKX | My referral code: paulbarronOKX United States - Sign up and log in to the OKX app to get exciting rewards. ➜ https://app.okx.com/en-us/join/paulbarron